The Oil Industry post peak demand and the Anna Karenina Principle

Most companies will be unhappy in their own way

All happy families are alike; each unhappy family is unhappy in its own way.

Leo Tolstoy, Anna Karenina

More widely, the Anna Karenina Principle states that a deficiency in any one of a number of factors can doom an entire endeavour to failure.

Introduction - Saudi Aramco – a cautionary tale part 1

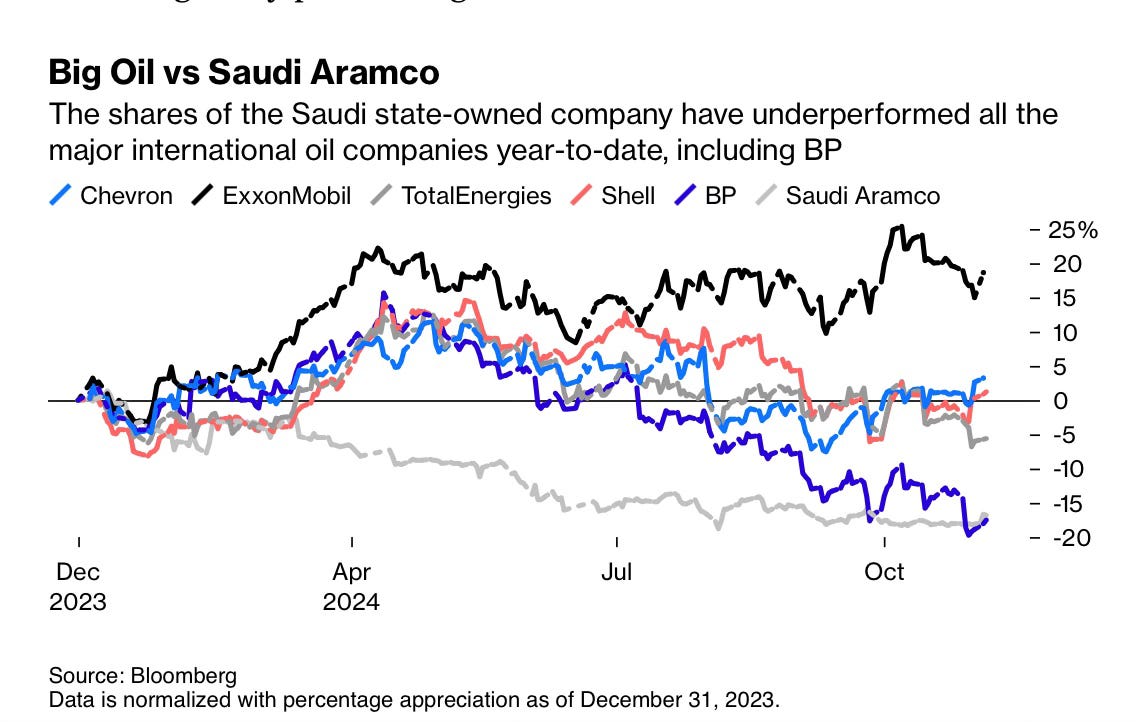

From Bloomberg this week:

“Saudi Aramco is taking on debt to sustain its dividend (that mostly goes to the government). In nine months, its position has moved from net cash of $27.4 bn to net debt of $8.9 bn. That means in 2024 Aramco has spent ~$130 million daily that it didn’t have.”

So far, so standard. Sometimes oil and gas companies borrow to pay dividends to keep shareholders sweet, assuming the good times will return, and meantime the share price has been buoyed.

But as we know the world of energy is changing and an oil demand peak may already be with us principally due to lower transport demand as it shifts to electrification, driven hard by massive exports of US and Chinese EVs.

Many note that this peak may just mean a plateau for a while, so plenty of time for adjustment.

Well – turns out that depends.

We have to look a wee bit harder into the oil demand and supply story to understand how that peak now takes away one major dimension of freedom that oil companies assumed they would always have – increasing demand.

We’ll come back to Aramco’s particular issues in a moment

Meanwhile, let’s take a step back

The oil industry and the Anna Karenina Principle

Let’s assume in the next year or two that demand peak is a reality.

You enter the new strange world of constrained arithmetic.

Demand has met a celling, and one that is now slowly but firmly dropping

So your ability to produce more oil has now become a lot more constrained – this is the world OPEC has been operating under for over 10 years, curbing its vast potential energy supply to maintain prices.

In the interim this faux demand – supply gap has been filled by IOCs, so in reservoir reality supply vastly outstrips demand, but in trading and commodity reality supply is constrained so the market is willing to pay extra to get its oil.

Of course, this describes the oil market for the last 50 years with many ups and downs – sometimes supply shocks through wars force the prices up for a bit and demand reduces, sometimes demand falters eg in COVID and the market has to re-adjust by paring supply.

An equilibrium of sorts is always eventually achieved, but at the cost of volatile oil prices, inflation and all the political hinterland that infects.

The key to this precarious existence is the fluidity of supply and demand against an overall setting of demand growth, which allows adjustments and course corrections to meet the yearly mood, and re-set into the pattern of expansion.

But oil supply and oil demand are asymmetric phenomena.

Supply is a fixed commodity of crude oil, it is finite, reserves today will meet about 50 years of current demand, and at a stretch depending on price and environmental impact perhaps 75 years. Still finite, but more a long-term risk to manage.

Demand however is a vast array of end uses and products and materials. It is guessed at via the implied supply required. So sudden shifts in behaviour or technology far removed from offshore oil-fields can quite suddenly shift the equation.

So far, year on year changes can be accommodated as long as the long term trends are long term supply in place, long-term demand growing.

What happens when the second of these is reversed?

Long-term supply in place, long-term demand declining – and as we have noted this is likely now the case, so it is not hypothetical.

Many writers suggest “so what, as the market will still balance”.

But the muscle memory of the oil and gas industry is too strong and will likely over-ride market rationality: at near-peak demand and even after peak is confirmed, it will still feed the supply machine with new production - even as OPEC holds back as it sees the demand cliff-edge arrive.

To be clear, when peak demand arrives there will be no bell rung, or a bright firework display.

But it will still have peaked, and each oil company international and national of all sizes will reach that same singular peak together, but with their own very particular business conditions.

Imagine a presentation in each oil HQ which highlights here is our business position at now near peak, and here is where we will be 5 years after it.

Fantasy of course, because oil companies do not prepare for such a day in this way, nor entirely believe it will happen anyway (the grizzled realists).

Because almost all will prefer to react to the peak, and not pre-empt it – for that is what experienced players do especially in an engineering industry. Better to respond to hard reality than imagine and prepare for an abstract event.

Nevertheless, what is almost certain is that every oil and gas firm will look very different on peak day.

So how will each fare after the peak ?

All fine, all doomed ? Literature may hold a clue

You can label it the Oil and Gas Anna Karenina principle: successful oil and gas companies are alike, each unsuccessful one unsuccessful in its own way.

The wider principle Tolstoy saw is that a deficiency in any one of a number of factors can doom an entire endeavour to failure.

So although each oil and gas company is prey to the vagaries of supply / demand and so price – there is the third dimension of their personal business model and circumstance, and how well it matches the world when the lights go out on demand growth.

Peak demand is such a systemic shock that it will almost immediately stress test each firm’s business situation by hunting down any deficiency it has.

And we don’t have to wait for the bell-ringing peak-day to arrive: as we close in on peak demand, many firms, especially OPEC, have already had to decelerate and stop production growth as if it were already here. Right now.

How are oil firms doing in the shadow of the peak ?

Saudi Aramco – a cautionary tale part 2

Let’s take the biggest of them all, Saudi Aramco, and try to figure out why it is in such sudden financial discomfort as detailed at the top of the note.

If we assume for a minute global peak oil demand, that background of growth now gone, we can concentrate on specific Aramco supply and business model issues.

First supply: Aramco has a self-imposed production supply target of 9 million b/d to meet its OPEC quota in light of global diminishing demand.

In turn that forces it to have a revenue solely determined by oil prices – blunt arithmetic (barrels x $ /barrel).

In 2024 oil prices have fallen about 10%, and thus so have Aramco’s revenues. It still posts healthy profits, but it turns out this does not matter because of its business model.

Business model: Saudi Aramco and the Kingdom of Saudi Arabia are essentially the same thing: it is the very essence of a petro-state, governed, beholden and focussed on oil production for revenues. Aramco is Saudi Arabia, Saudi Arabia is Aramco.

To fund the state’s goal (Project 2030) to try and diversify to handle the needs of a burgeoning population (having doubled to 32 million since 2000), Aramco has a fixed dividend ($20bn per quarter) it needs to pay to the state, irrespective of market conditions to fund non-oil ventures.

On top of this, due to putting its toe in the waters of the world energy markets with a share release, another dividend based on performance has been added to the base to satisfy international investors.

How does this seemingly straightforward model lead to Bloomberg’s comment that Aramco needs to “stop burning cash”.

Let’s boil that down to two simple numbers – free cash flow (money left to spend from income after taxes, capital expenditure etc), and the cost of these dividends, and compare 2023 and 2024 YTD (Sept 2024).

2023 YTD – Free Cash $74 bn , Dividends $68 bn ; Net Cash $6bn surplus

2024 YTD – Free cash $64 bn , Dividends $93 bn ; Net Cash - $(29bn) debt

In fact, to extrapolate lightly, for full year 2024 Aramco expect dividends of $124bn, against free cash flow estimate of ca $84bn, meaning a negative debt requirement of $40bn.

Aramco has a very strong balance sheet, but this sort of business model is unsustainable even for them, and another year of it would likely have them breach their own gearing targets of 5-15%, territory they have rarely ever been in. Yet may be committed too.

However they have no ability to increase production (and revenues) due to their OPEC+ commitments, and as demand declines overall, oil prices seem set to fall further. The revenue side of their equation is capped, and likely to fall due to prices, but their dividend exposure is fixed for now.

Aramco is squeezed between this falling ceiling, and a very hard floor.

To chisel out the floor, and cut the base and performance dividends only signals to the market their business model has key deficiencies and stock price and market capitalisation will fall. As it has done as we will see.

Let’s leave Aramco to their floor and ceiling fate there, it is theirs to manage to avoid dooming their endeavour to failure.

If we switch to the broader view, this cautionary tale highlights three major themes for the oil industry ahead.

As peak occurs, most oil and gas companies will be unhappy in their own way

1 – Peak oil demand is not an incident or occurrence: it is a systemic signal of a change in the oil industry environment.

As the Aramco tale shows, when the peak is confronted it is clear one key dimension of standard business reaction – production growth – is not taken away intermittently, but for good.

Any oil firm encountering this transition from hoped-for growth, to constant decline, has to quickly review their business model for deficiencies – whether locked-in dividends, or locked-in plans for expansion or other investments.

Aramco has over-committed dividends and capped supply, so theirs is an exquisite pain to address. But all the others will have their own particular shortcomings to see to.

2 The industry supply problem - all firms have their own unhappy business structures to address whether over-expansion or high operating costs.

But as a group, the oil industry has already built in one aggregate deficiency: as OPEC+ curbed supply, all other oil firms dis not restrain in tandem: some did but overall the industry is set for capital expansion, and production expansion, at a time when demand drops.

When the light dims on demand growth, all these business models will have a sudden spotlight trained on them from many other directions such as markets and governments.

If they look over the wall to their counterparts in the car transport industry they will see carnage as demand for oil-fired cars has disappeared almost overnight, and major brands such as BMW, Nissan and Toyota are staring to collapse in value.

If this is news to any oil executive, then the oil company he or she runs has a deficiency that may doom the endeavour.

3 – The dimensions of industry freedom are suddenly disappearing. With demand at a peak, the ability to produce more disappears and prices also decline.

Two key dimensions have gone almost instantly in industry timescales; production growth and higher prices cannot now ever be assumed.

All business models built to assume lower production and lower prices should be happy ones: each one that doesn’t will be unhappy in its own way, whether by over-committing dividend, capital or growth. Or many others.

Given the oil and gas industry culture and attitude to change, it is likely the peak spotlight finds them all unready for disruption, and then unhappy in their own way.

The Oil Industry post peak demand and the Anna Karenina Principle – most companies will be unhappy in their own way